Management of state-owned assets in administrative institutions

State-owned assets of administrative institutions refer to all kinds of economic resources that are occupied and used by administrative institutions, legally recognized as owned by the state and can be measured in money. It is an important material basis for the government to perform social management functions, provide public services and promote career development, and is an important part of state-owned assets.

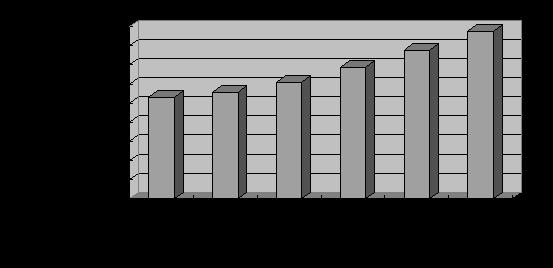

(1) the status quo of state-owned assets in administrative institutions. According to the data of final accounts of departments in 2011, as of December 31, 2011, the total assets of administrative institutions nationwide were 13.35 trillion yuan, and the total net assets after deducting liabilities were 8.76 trillion yuan. The net assets of administrative institutions accounted for about one-third of the total state-owned net assets (see Figure 5.1). In terms of asset composition, current assets account for 40.3%, fixed assets account for 50.2%, foreign investment accounts for 1.8%, intangible assets account for 0.5%, and other assets account for 7.2% (see Figure 5.2).

Figure 5.1 State-owned Assets of Administrative Institutions in 2006-2011 (Net Value)

Figure 5.2 Composition of state-owned assets (total value) of administrative institutions at the end of 2011

(2) State-owned assets management system of administrative institutions. In 2006, the Ministry of Finance promulgated the Interim Measures for the Management of State-owned Assets in Administrative Units and the Interim Measures for the Management of State-owned Assets in Public Institutions (Ministry of Finance Orders No.35 and No.36, hereinafter referred to as "two ministerial orders"), which clarified the management system of state-owned assets in administrative institutions and the management responsibilities of various departments (units), comprehensively standardized the management of assets allocation, use and disposal, and constructed a comprehensive management system from asset allocation, use to disposal. According to the relevant principles determined by the two ministerial decrees, the Ministry of Finance, in conjunction with relevant departments, has studied and promulgated relevant supporting management measures such as asset inventory, asset verification, state-owned assets management of central administrative institutions, overseas assets management and the use, disposal and income of state-owned assets. At the same time, local financial departments have actively strengthened the system construction according to the provisions of the two ministerial orders, and the state-owned assets management system of administrative institutions has been initially established.

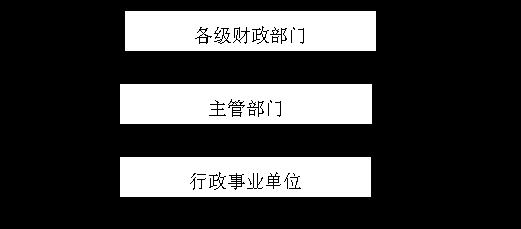

(3) State-owned assets management institutions of administrative institutions and their responsibilities. According to the current management framework of state-owned assets in administrative institutions, it is vertically divided into five levels: central, provincial, prefecture (city), county and township, and horizontally there are three levels of management: "financial department-competent department-administrative institutions".

The specific responsibilities and authorities of financial departments, competent departments of administrative institutions (hereinafter referred to as competent departments) and administrative institutions in asset management are as follows: financial departments at all levels are government functional departments responsible for the management of state-owned assets of administrative institutions and implement comprehensive management of state-owned assets of administrative institutions; The competent department is responsible for the supervision and management of the state-owned assets of the administrative institutions affiliated to this department; Administrative institutions shall implement specific management of the state-owned assets possessed and used by their own units.

The promulgation of the two ministerial orders clearly defined the management system of state-owned assets in administrative institutions in China. At present, the management system of "unified ownership by the state, graded supervision by the government, possession and use by units" and the corresponding state-owned assets management model of "financial department-competent department-administrative institution" have been further established nationwide. By the end of 2011, all provinces (autonomous regions, municipalities directly under the Central Government and cities with separate plans) in China have made it clear that the financial departments are responsible for the management of state-owned assets in administrative institutions, and 35 of them have established special asset management institutions. Most central departments have also set up asset management institutions or defined the staff responsible for asset management.

(4) The main contents of state-owned assets management in administrative institutions. It mainly includes asset allocation, asset use, asset disposal and other related work.

Asset allocation. It refers to the behavior of financial departments, competent departments, administrative institutions, etc. to equip administrative institutions with assets by means of purchase or adjustment according to the needs of administrative institutions to perform their functions and in accordance with the procedures stipulated by relevant state laws, regulations and rules. Administrative institutions purchase assets included in the scope of government procurement and implement government procurement according to law. In order to standardize and strengthen the asset budget management, the Ministry of Finance issued the Notice of the Ministry of Finance on Further Strengthening the Budget Management of New Asset Allocation in Central Administrative Units (Caixing [2010] No.293) and the Budget Standard for the Purchase of General Office Equipment and Furniture in Central Administrative Units (for Trial Implementation) (Caixing [2011] No.78) to standardize the asset budget preparation of central departments and improve the budget for the purchase of general office equipment and furniture in central administrative units.

Use of assets. Including assets for self-use, foreign investment, leasing and lending. Administrative institutions shall establish and improve the management system for the use of state-owned assets, standardize the use behavior, do a good job in the use management, give full play to the use efficiency of state-owned assets, ensure the safety and integrity of state-owned assets, and prevent improper losses and waste in the use of state-owned assets. Administrative units shall not use state-owned assets as external guarantee, and shall not use state-owned assets in any form to hold economic entities. The income from leasing and lending of state-owned assets in administrative institutions shall be managed by "two lines of revenue and expenditure" in accordance with the provisions of the government on the management of non-tax income. The income from the use of state-owned assets in public institutions should be included in the unit budget, and unified accounting and management should be carried out.

Disposal of assets. Refers to the transfer and write-off of property rights of state-owned assets in administrative institutions. Including all kinds of state-owned assets free allocation (transfer), foreign donation, sale, transfer, transfer, replacement, loss reporting and scrapping, loss verification of monetary assets, etc. The income from the disposal of state-owned assets in administrative institutions shall be managed by "two lines of revenue and expenditure" in accordance with the provisions of the government on the management of non-tax income.

Other basic work. It mainly includes supporting basic work such as asset inventory, asset verification, property right registration and asset evaluation of administrative institutions, and constitutes the content system of asset management of administrative institutions with three basic links of asset allocation, use and disposal.

Approval process. Administrative institutions at all levels shall, in strict accordance with the relevant provisions of the state, go through the formalities for examination and approval of asset allocation, use and disposal, and follow the process shown in Figure 5.3 for approval.

Figure 5.3 Schematic diagram of approval process

(5) Special management of state-owned assets in administrative institutions.One isOfficial vehicle management. The Ministry of Finance issued the Administrative Measures for the Budget and Final Accounts of Official Vehicles for Party and Government Organs (No.9 [2011] of Caixing) and the Administrative Measures for the Equipment and Use of Official Vehicles for Law Enforcement of Party and Government Organs (No.180 [2011] of Caixing), and formulated the Administrative Measures for the Equipment and Use of Official Vehicles for Law Enforcement of Sub-systems together with the central competent authorities, further put forward management requirements for the budget and final accounts of official vehicles for Party and government organs, and set the equipment scope, preparation management and equipment standards for official vehicles for law enforcement of party and government organs.The second isSoftware asset management. In order to further improve the use of legitimate software by government agencies, the Ministry of Finance issued the Notice on Further Standardizing and Strengthening the Management of Software Assets of Government Agencies (Caixing [2011] No.7), which put forward clear requirements on budget management, asset management and procurement management of legitimate software, standardized and strengthened the management of software assets of government agencies, and promoted the protection of intellectual property rights.